| Western Asset Prem Inst Liq Res Cap (WAAXX) | 5.42 |

| DWS ESG Liquidity Inst (ESGXX) | 5.40 |

| State Street Inst Liq Reserve Prem (SSIXX) | 5.39 |

| Allspring Heritage Select (WFJXX) | 5.37 |

| Federated Hermes Inst MM Mgmt IS (MMPXX) | 5.36 |

| Invesco Premier Investor (IMRXX) | 5.37 |

| First American Ret Prime Obligs X (FXRXX) | 5.36 |

| Allspring MMF Prm (WMPXX) | 5.35 |

| UBS Prime Preferred Fund (UPPXX) | 5.34 |

| Federated Hermes Prime Cash Oblig WS (PCOXX) | 5.34 |

| Federated Hermes Muni Obligs WS (MOFXX) | 4.11 |

| Vanguard Municipal MMF (VMSXX) | 4.07 |

| Fidelity Inv MM: Tax Exempt I (FTCXX) | 3.97 |

| BlackRock Liq MuniCash Inst (MCSXX) | 3.93 |

| UBS Tax-Free Preferred (SFPXX) | 3.88 |

Money Market News

MORE NEWS »

ICI's latest "Money Market Fund Assets" report shows money market mutual fund assets rebounding after falling sharply the prior week due to tax payments. MMF assets are up by $91 billion, or 1.9%, year-to-date in 2024 (through 4/24/24), with Institutional MMFs down $20 billion, or -0.6% and Retail MMFs up $111 billion, or 6.6%. Over the past 52 weeks, money funds have risen by $715 billion, or 13.6%, with Retail MMFs rising by $502 billion (26.4%) and Inst MMFs rising by $262 billion (7.9%). (Note: Thanks to those who visited with us at the `The New England AFP Annual Conference!)

Inside Money Fund Intelligence

MFI PDF April 2024 Issue |

Largest Money Fund Managers |

|

|

The April 2024 issue of Money Fund Intelligence features: "Pending Reforms Trigger Prime Shift: Federated, Vanguard Go," which covers the budding exodus from Prime Institutional MMFs; "Bond Fund Symposium '24: Ultra-Shorts Look for Bounce," which quotes from our recent ultra-short bond fund conference; and, “Worldwide MF Assets Break $10 Trillion in '23; US Leads," which reviews ICI's latest global money fund statistics. Each monthly issue of Money Fund Intelligence features news, performance information and rankings on money market mutual funds. Statistics include: assets, weighted average maturity, weighted average life, expense ratio, 7-day yield, 30-day yield, 1-year, 3-yr, 5-yr, 10-yr, and since inception return, as well as 7- and 30-day gross yields. MFI also contains tables of the top-yielding and the largest money funds, and our benchmark Crane Money Fund Indexes. Subscriptions are $500 a year, and include online access to archived issues and additional features. Bulk discounts and site licenses are available. Write info@cranedata.com or call 1-508-439-4419 to subscribe or to request more information. |

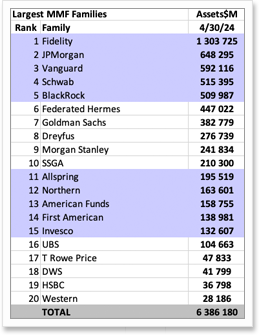

The table below is excerpted from our monthly spreadsheet product, Money Fund Intelligence XLS. It shows the largest money market mutual fund managers as of March 31, 2024. (MFI XLS contains percentile rankings, fund family rankings, MNAVs, WLA, portfolio composition, and more).

|

|

About Crane Data LLC

Crane Data is a money market and mutual fund information company founded by Peter G. Crane and Shaun Cutts. We collect money market mutual fund, bank savings, and cash investment performance, statistics, and information and distribute rankings, news, and indexes.

Crane Data publishes Money Fund Intelligence, Money Fund Intelligence XLS, Money Fund Wisdom, the Crane Money Fund Indexes, and a series of products tracking money markets, mutual funds and cash investments. We also produce conferences, including Crane's Money Fund Symposium. For more information and samples, e-mail info@cranedata.com or call us at 1-508-439-4419.

Link of the Day

MORE LINKS »

Apr 26

Fed Posts Financial Stability Report

The Federal Reserve Board published a "Financial Stability Report" recently, which comments on "Funding Risks," "Vulnerabilities from funding risks remained notable, reflecting challenges at some banks and structural vulnerabilities in other sectors engaged in liquidity transformation. The banking industry maintained a high level of liquidity since the October report. Funding ...

People

more »

Apr 24

Birdthistle Out at SEC; Vij Greiner In

A press release tells us, "The Securities and Exchange Commission ... announced that William Birdthistle, the Director of the Division of Investment Management, will depart the agency.... Natasha Vij Greiner, currently the Deputy Director of the Division of Examinations, will be named Director of the Division of Investment Management."

Mar 04

GLMX Promotes Giglio and Wiblin

A release titled, "GLMX Promotes Giglio and Wiblin as Expansion Continues" says, "GLMX, a comprehensive global technology solution for trading Money Market instruments, including repurchase agreements, ... announced [that] Sal Giglio, previously COO and Chief Markets Officer, has been promoted to President and Chief Revenue Officer. Andy Wiblin, previously Chief Product Officer, has been promoted to Global Chief Operating Officer."

Feb 26

Straker Moves to Federated Hermes

Jason Straker is now a VP & Senior Sales Representative with Federated Hermes. He was previously with Western Asset.

Crane Data News & Features

contact us »Money Fund Symposium Pittsburgh, 6/12-14

Get ready for Crane Data’s big show! Money Fund Symposium will be held June 12-14, 2024, in Pittsburgh, Pa. Register and make hotel reservations soon. Also, thanks to those who attended our recent Bond Fund Symposium in Philadelphia! Next year's BFS will be held March 27-28, 2025 in Newport Beach, Calif. Mark your calendars for our European Money Fund Symposium, which will be in London, Sept. 19-20, 2024, and our Money Fund University, which will be in Providence, Dec. 19-20, 2024. Conference recordings and materials are available at the bottom of our "Content" page. Watch for more details on future shows in coming months, and let us know if you'd like more information. We hope to see you in Pittsburgh in June, in London in September or in Providence in December 2024!